Italian imports of plastics and rubber processing machinery racked up an impressive 23% increase in the first half of 2018 with regard to the same period in 2017. On the other hand, the growth of exports is instead fractional, evidencing the lacklustre performance heralded in the early months of the year. While still well into the black at over one billion euros, the balance of trade has bogged down somewhat, losing over 7%. This is the situation captured by the statistical studies centre of Amaplast based on foreign trade data published by Istat.

The dynamism of purchases from abroad may be interpreted as renewed faith in the domestic market, mainly due to investment incentives that are likely to be renewed and naturally hoped for by businesses in the industry.

Among the main machinery categories, the greatest gains are recorded for imports of injection moulding machines (+31%) and blow moulding machines (+75%), accompanied by flexographic printers (+111%) and moulds (+12%). Some of the sources of this performance may be found in the positive trend in the Italian packaging industry - the principal consumer of plastic raw materials and processing machinery - as also determined by the Italian packaging machinery manufacturers association (Ucima). This latter observed growth of over 14% in 2017 for packaging companies in the domestic market, with the results for the current year also expected to show positive performance.

The principal supplier country for the Italian plastics and rubber processing industry is Germany, which has significantly improved its leading position with respect to the period January-June 2017, widening its gap over China, in second place.

Germany also maintains its status, one which it has held for decades, as the main destination for Italian exports in the sector, evidencing the continuing faith of German customers in Italian-made technology.

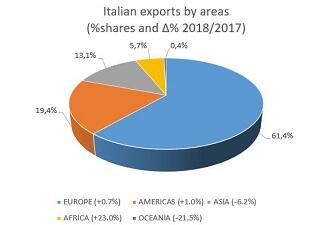

A broad look at the geography of exports shows:

- the primacy of Europe as a whole, with some 61% of the total, remaining substantially unvaried with respect to the first half of 2017, with growth over other markets measured in decimals. This stasis is mainly due to a falloff of sales to Russia (-32%) after the hope-inspiring recovery in 2017; enthusiasm has definitely waned in the first half of this year;

- good performance in exports to the three Nafta countries (+7%), placing North America in second place among export destinations, counterbalanced to some extent by the overall contraction of Central and South American markets;

- an overall slowdown in Asia (-6%), mainly deriving from weak sales in the Middle East;

- positive progress in Africa (+23%), thanks to increased sales both to Mediterranean and

Sub-Saharan countries;

- weakening (-21%) in the already modest supplies to the distant markets of Oceania.

As regards goods categories, positive growth in exports is observed for all principal types of primary transformation machinery and moulds, which together account for more than half of the sector’s sales abroad.

The

commercial balance is in the black across the board, with the sole exception of

injection moulding machines, which have slipped into ![]() negative territory by

about 14 million euros.

negative territory by

about 14 million euros.

Amaplast President Alessandro Grassi (picture right) comments on the most recent end-of-period sentiment survey completed at the beginning of September by the association’s statistical studies centre: “The July order books for Amaplast member manufacturers are stable with a slight trend toward improvement - with respect to both June 2018 and July 2017 - and this gives us reason to hope for a rebound in production and exports in the last quarter of the year”.

Notizie più lette